The financial management of Homa Bay County has recently gained attention, not for commendation, but due to significant inefficiencies and mismanagement issues being brought to light.

The Auditor-General’s latest report reveals a series of alarming discrepancies and administrative failures that underscore the extent of the rot within the county’s fiscal operations.

This article delves into the critical findings that highlight the dismal state of financial governance in Homa Bay County.

Under the leadership of Governor Wanga, officials voided 516 transactions totaling Shs 1.4 billion in the years 2022–2023. [PHOTO: Nairobi News]

Gladys Wanga, the governor of Homa Bay, has garnered praise for initiating numerous high-profile projects in South Nyanza County. However, beneath this veneer of success, there are significant allegations of corruption and mismanagement within her administration.

Reports suggest that the executive branch under her leadership is embroiled in activities that violate procurement laws, lack accountability, and engage in substantial looting.

Key projects touted by Governor Wanga, such as the landscaping and driveway works at Kigoto Milling Plant and the construction of staff houses at God Agulu Health Center, have reportedly stalled.

These issues raise serious concerns about the actual effectiveness and integrity of her administration’s operations.

Despite the positive media coverage and public accolades, the underlying issues of corruption and project mismanagement point to a need for greater scrutiny and accountability in her government’s practices.

The discrepancy between the public image of progress and the reality of stalled projects and corruption allegations highlights a critical need for transparency and effective governance to ensure that development goals are genuinely met and public resources are used responsibly.

Discrepancies in Transfers from the County Revenue Fund (CRF)

The county’s financial statements reflect transfers from the County Revenue Fund amounting to Kshs 8,294,677,144. However, the financial statement for the CRF itself shows transfers totaling Kshs.8,290,443,769, resulting in an unexplained variance of Kshs. 4,233,375.

This discrepancy casts doubt on the accuracy and completeness of the reported transfers, suggesting potential manipulation or gross oversight in financial reporting.

Unsupported Adjustments to Financial Statements

Significant revisions were made to the county’s financial statements between their initial submission in September 2023 and their resubmission in February 2024.

These revisions included adjustments to other grants and transfers from Kshs. 414,272,635 to Kshs. 282,717,338 and changes in the Financing Locally Climate Action Programme Led (FLOCA) from Kshs. 16,000,000 to Kshs. 9,286,362.

However, these adjustments lacked supporting documentation, such as approved journal entries and expenditure schedules, raising serious concerns about their legitimacy and transparency.

Inaccuracy in Transfers to Homa Bay Municipality Board

The financial statements report transfers to the Homa Bay Municipality Board amounting to Kshs.3,500,000, while the municipality’s own records show receipts totaling Kshs.22,281,737. This staggering variance of Kshs.18,781,737 remains unexplained, pointing to either severe mismanagement or potential misappropriation of funds.

Pending Accounts Payable and Undisclosed Debts

Homa Bay County has pending accounts payable amounting to Kshs. 955,548,525, with Kshs. 882,328,436 carried over from the previous year in violation of financial regulations.

Additionally, the county executive owes the Kenya Revenue Authority Kshs. 1,913,856,589, a liability conspicuously absent from the financial disclosures.

This failure to settle and accurately report debts distorts financial statements and hampers effective budgetary planning.

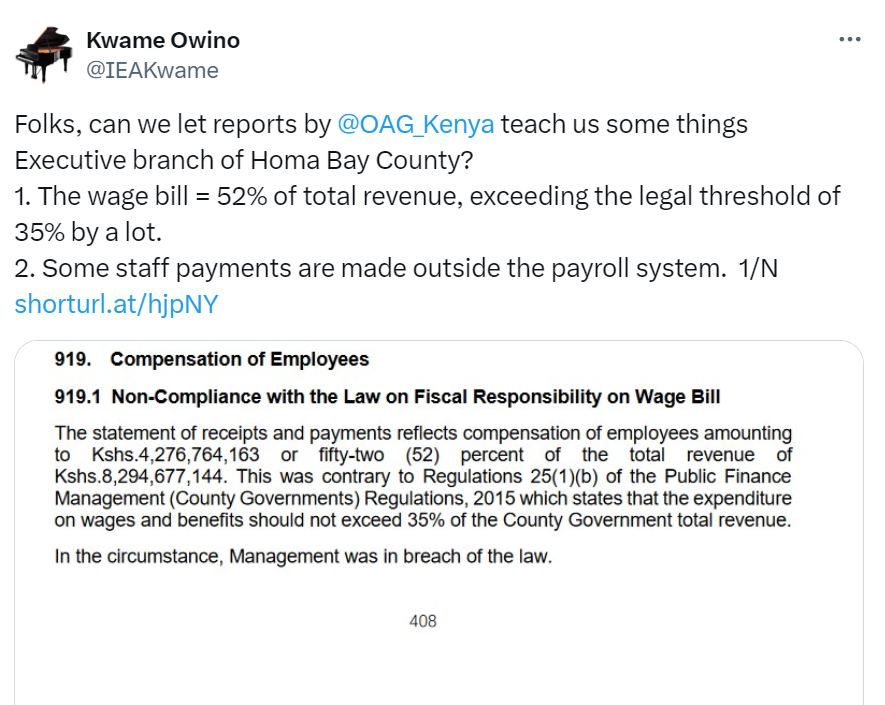

Breach of Law in Compensation of Employees

The county’s wage bill stands at Kshs. 4,276,764,163, which is 52% of its total revenue, far exceeding the legally mandated limit of 35%.

Furthermore, Kshs. 8,104,029 was processed manually outside the Integrated Payroll and Personnel Database (IPPD) system, contravening national treasury regulations.

These breaches not only reflect fiscal irresponsibility but also expose the county to risks of fraud and payroll inconsistencies.

Misuse and Lack of Accountability in Expenditure

Several expenditures under the use of goods and services, amounting to Kshs. 971,136,710, are riddled with irregularities:

Irregular Payments to the Council of Governors: Kshs 5,850,000 was spent on subscriptions, despite such expenses being the responsibility of the National Government.

Unsupported Consultancy Fees: Payments totaling Kshs. 2,950,000 and Kshs. 38,886,000 for environmental assessments and legal services, respectively, were made without requisite documentation, questioning their validity and value for money.

Infrastructure Projects: Incomplete and Mismanaged

The county’s acquisition of assets, reported at Kshs. 2,076,703,613, is marred by incomplete projects and substandard work:

Kigoto Maize Milling Plant: Multiple infrastructure projects, including landscaping and borehole installation, remain unfinished despite significant expenditure.

County Stadium and Health Facilities: Major projects like the Homa Bay Stadium and various health facilities are incomplete or stalled, reflecting poor project management and possible misappropriation of funds.

Governance Failures

The report also highlights systemic governance failures:

Lack of Staff Establishment and ICT Policy: The absence of an approved staff establishment and ICT policy undermines the county’s operational efficiency and data integrity.

Lack of an Assets Register and Audit Committee: The county’s inability to maintain an accurate asset register and the absence of an audit committee compromise the management and oversight of county resources.

Governor Gladys Wanga has failed to implement budgeted projects in Homa Bay. Her administration lacks an Asset Register, an ICT policy, and an Audit Committee.

Under her leadership, officials voided 516 transactions totaling Shs 1.4 billion in the year 2022–2023. Despite her high-profile announcements, corruption and mismanagement are rampant in her government.

Conclusion

The Auditor-General’s report paints a grim picture of Homa Bay County’s financial health, marked by irregularities, non-compliance with financial regulations, and gross mismanagement of public resources.

The county leadership must urgently address these issues, enforce strict financial controls, and ensure accountability to restore public trust and effectively serve its citizens.

The citizens of Homa Bay deserve transparency and efficiency, not the fiscal mismanagement that currently plagues their county.